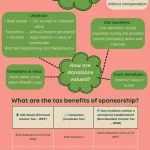

Tax incentives for sponsorship in Spain

Spain offers a favourable tax regime for sponsorship, allowing significant deductions in Personal Income Tax, Corporate Tax and even in wealth-related taxes such as Inheritance and Gift Tax.

Spain offers a favourable tax regime for sponsorship, allowing significant deductions in Personal Income Tax, Corporate Tax and even in wealth-related taxes such as Inheritance and Gift Tax.

Comparison of the legal and tax implications of the Beckham and Mbappé regimes, their main advantages, and the eligibility requirements for each.

There are different reasons why a company can be subject to a tax inspection: excessive VAT refunds, discrepancies between quarterly and annual models (…), or commonly for random reasons.

Non-resident companies that own real estate in Spain are subject to the non-resident income tax by means of a special tax payable on 31 December of each year and which must be paid in January of the following year.

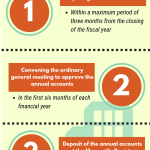

Read the full article: The Deposit of Annual Accounts in Spain

From 1 January 2017, large companies and professionals registered in the VAT Refund Special Regime will be required to use the new system for registering VAT books through the electronic office of the Spanish Tax Administration Agency.

One of the most important novelties introduced by the reform of the Law on Income Tax in Spain concerns the VAT taxation of a company’s partners engaged in professional activity.

The new fiscal reform in Spain, which will gradually be implemented in 2015 and 2016, will benefit rents bellow 50.000€ and individuals with family responsibilities. Severance pay shall be taxed, the exclusion of the dividends is abolished and the deductible quality of pension plans is reduced.

The Preliminary Law on Fiscal Reform in Spain is creating a much more effective business competition aimed at both self-employed workers and businesses. The Reform proposes changes to tax on companies (TC), tax on the income of individuals (TII), tax agency, and VAT regarding e-commerce.

The fiscal reform in Spain implies a lowering of tax withholdings for self-employed people whose annual income is lower than 12.000 €. Self-employed workers can benefit from these measures beginning on the 1st of July 2014.

© 2026 Mariscal Abogados, S.L.P.

Legal Notice | Privacy Policy | Cookies Policy